by Andrew Griffith, Livestock Marketing Specialist

August 7, 2026

Overview

Corn, Soybean, Wheat softer for the week with Cotton up a little

Fuel

Tennessee fuel prices were largely lower compared to last week. Current average prices stand at $3.60 per gallon for regular gasoline, $4.06 for mid-grade, $4.47 for premium, and $5.01 for diesel. Compared with one week ago, prices declined $0.10 per gallon for gasoline products and were unchanged for diesel, while current prices are $0.21 to $0.22 per gallon higher than one month ago for gas and $0.57 per gallon higher for diesel. The most significant changes are evident in the year-over-year comparison, with gasoline increasing $0.79 to $0.80 per gallon and diesel increasing $1.56 per gallon.

| Fuel | Regular | Mid-Grade | Premium | Diesel |

|---|---|---|---|---|

| Current Avg. | $3.60 | $4.06 | $4.47 | $5.01 |

| Yesterday Avg. | $3.62 | $4.08 | $4.49 | $5.04 |

| Week Ago Avg. | $3.70 | $4.16 | $4.57 | $4.57 |

| Month Ago Avg. | $3.38 | $3.85 | $4.26 | $4.26 |

| Year Ago Avg. | $2.80 | $3.27 | $3.67 | $3.67 |

| Indicator | Previous | Current | Change |

|---|---|---|---|

| USD Index | 100.04 | 99.95 | -0.09 |

| Crude Oil | 84.55 | 83.64 | -0.91 |

| DJIA | 52457 | 53885 | 1428 |

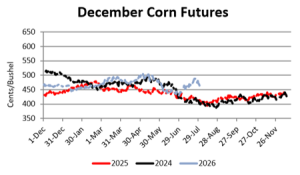

Corn

Across Tennessee, average corn basis (cash price-nearby futures price) declined 3 cents from last week at West, Northwest, West-Central, North-Central, and Mississippi River elevators and barge points. Overall, basis for the week ranged from 13 cents under to 10 cents over, with an average of 3 cents under the September futures at elevators and barge points. Ethanol production for the week ending July 31st was 1.107 million barrels, down 26,000 barrels compared to the previous week. Ethanol stocks were 24.524 million barrels, down 202,000 barrels compared to the previous week. Cash prices ranged from $4.27 to $4.54 at elevators and barge points. On Friday, September 2026 corn futures closed at $4.39, which is down 2 cents compared to last week. For the week, September 2026 corn futures traded between $4.37 and $4.49.

Nationally, the Crop Progress report estimated corn condition at 61% good-to-excellent (down 2% from last week) and 14% poor-to-very poor (up 2% from last week); corn dough to be 43% compared to 25% last week, 40% last year, and a 5-year average of 38%. In Tennessee, corn condition was estimated at 81% good-to-excellent (up 1% from last week) and 4% poor-to-very poor (down 1% from last week). This week new crop cash contracts ranged from $4.24 to $4.75 at elevators and barge points.For the week of July 24-30, 2026, net sales of 116,700 MT for 2025/2026–a marketing-year low–were down 68 percent from the previous week and 70 percent from the prior 4-week average. Net sales of 1,026,900 MT for 2026/2027 were primarily for unknown destinations (490,400 MT), Mexico (151,500 MT), South Korea (151,000 MT), Japan (60,000 MT), and Taiwan (39,100 MT). Exports of 1,925,500 MT were up 26 percent from the previous week and 14 percent from the prior 4-week average. December corn futures closed at $4.62, down 2 cents from last week.

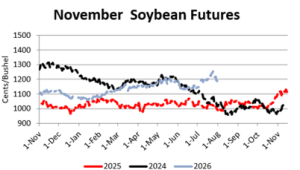

Soybeans

Across Tennessee average soybean basis increased 2 cents compared to last week at West, Northwest, North-Central, West-Central, and Mississippi River elevators and barge points. Average basis ranged from 40 under to 10 cents over the August futures contract, with an average basis of 23 cents under at the end of the week. Cash soybean prices at elevators and barge points ranged from $11.16 to $12.05. September 2026 soybean futures closed at $11.57, down 15 cents compared to last week. For the week, September 2026 soybean futures traded between $11.52 and $11.69.

Nationally, the Crop Progress report estimated soybean condition at 63% good-to-excellent (no change from last week) and 9% poor-to-very poor (no change from last week); soybean setting pods to be 62% compared to 47% last week, 56% last year, and a 5-year average of 55%. In Tennessee, soybean condition was estimated at 75% good-to-excellent (no change from last week) compared to 9% poor-to-very poor (down 1% from last week); setting pods to be 78% compared to 70% last week, 55% last year, and a 5-year average of 56%. Net sales of 32,200 MT for 2025/2026–a marketing-year low–were down 89 percent from the previous week and 79 percent from the prior 4-week average. Net sales of 903,900 MT for 2026/2027 were primarily for unknown destinations (497,500 MT), China (330,000 MT), Mexico (45,000 MT), Colombia (10,000 MT), and Vietnam (6,100 MT). Exports of 346,000 MT were down 29 percent from the previous week and 24 percent from the prior 4-week average. November 2026 soybean futures closed at $11.76, down 12 cents compared to last week.

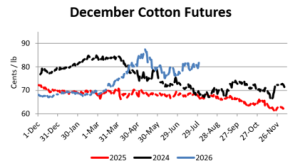

Cotton

North Delta upland cotton spot price quotes for August 6th were up compared to last week. Prices were 78.21 cents/lb (41-4-34), and 82.96 cents/lb (31-3-35), which made both up 2.75 cents compared to last week’s prices.

Nationally, the Crop Progress report estimated cotton condition at 42% good-to-excellent (down 4% from last week) and 20% poor-to-very poor (up 4% from last week); setting bolls to be 55% compared to 45% last week, 53% last year, and a 5-year average of 56%. In Tennessee, the Crop Progress report estimated cotton condition at 57% good-to-excellent (down 4% from last week) and 16% poor-to-very poor (same as last week); cotton setting bolls to be 82% compared to 74% last week, 56% last year, and a 5-year average of 64%. Net sales reductions of Upland totaling 55,900 RB for 2025/2026–a marketing-year low–were down noticeably from the previous week and from the prior 4-week average. Net sales of 8,300 RB for 2026/2027 were reported for India (7,200 RB), Thailand (700 RB), Indonesia (200 RB), Japan (100 RB), and Mexico (100 RB). Exports of 5,000 RB were up 11 percent from the previous week, but down 35 percent from the prior 4-week average. For the week, December 2026 cotton futures closed at 83.16 cents, up 1.51 cents compared to last week. March 2027 cotton futures closed at 85.23 cents, up 1.97 cents compared to last week.

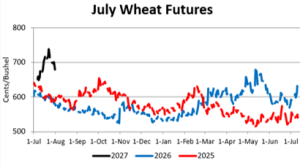

Wheat

Wheat cash prices at elevators and barge points ranged from $5.69 to $6.31.

Nationally, the Crop Progress report estimated spring wheat headed to be 98% compared to 92% last week, 95% last year, and a 5-year average of 97%. The report estimated winter wheat harvested to be 86% compared to 81% last week, 85% last year, and a 5-year average of 86%. Net sales of 296,400 metric tons (MT) for 2026/2027 were up 4 percent from the previous week and 6 percent from the prior 4-week average. Increases primarily for the Philippines (87,800 MT), Mexico (68,700 MT), Vietnam (62,000 MT), Thailand (43,600 MT), and unknown destinations (11,000 MT), were offset by reductions for Haiti (1,200 MT), Egypt (800 MT), and Trinidad and Tobago (700 MT). Exports of 419,000 MT were up 31 percent from the previous week and 46 percent from the prior 4-week average.

Additional Information

Links for data presented:

U.S. Export Sales – https://apps.fas.usda.gov/export-sales/esrd1.html

USDA FAS: Weekly Export Performance Indicator – https://apps.fas.usda.gov/esrquery/esrpi.aspx

EIA: Weekly ethanol Plant Production – https://www.eia.gov/dnav/pet/pet_pnp_wprode_s1_w.htm

EIA: Weekly Supply Estimates – https://www.eia.gov/dnav/pet/pet_sum_sndw_a_EPOOXE_sae_mbbl_w.htm

Upland Cotton Reports – https://www.fsa.usda.gov/FSA/epasReports?area=home&subject=ecpa&topic=fta-uc

Tennessee Crop Progress – https://www.nass.usda.gov/Statistics_by_State/Tennessee/Publications/Crop_Progress_&_Condition/

U.S. Crop Progress – http://usda.mannlib.cornell.edu/MannUsda/viewDocumentInfo.do?documentID=1048

USDA AMS: Market News – https://www.ams.usda.gov/market-news/search-market-news

If you would like further information or clarification on topics discussed in the crop comments section or would like to be added to our free email list please contact me at agriff14@utk.edu.